INTRODUCTION

9 Unbelievable Ways People With Tiny Salaries Save More in April Than You (The Hidden Rule You’re Ignoring)

Imagine checking your bank account in April and seeing a fat deposit, while your six-figure-earning neighbor gets zilch or even owes money.

It happens every year.

People scraping by on modest paychecks often walk away with bigger refunds or stash away more cash in April than folks earning double or triple that.

The hidden rule? It’s not luck, it’s a mix of smart habits, tax credits, and mindset shifts that high earners overlook.

And right now, with 2026 tax season in full swing, you can steal their playbook before the April 15 deadline hits.

Why Tiny-Salary Savers Often Beat High Earners in April

Here’s the shocker: Data from the IRS shows lower-middle income filers (around $15K–$20K) frequently pull in refunds that punch above their weight class, sometimes averaging more than brackets earning $30K–$50K.

Why? Refundable credits like the Earned Income Tax Credit (EITC) act like a built-in savings booster, designed exactly for them. High earners, meanwhile, face phase-outs, lifestyle creep, and over-withholding surprises that drain potential savings.

This isn’t about income envy. It’s about the hidden rule most people ignore: forced discipline plus targeted incentives equals bigger April wins.

People with tiny salaries live in a world where every dollar counts, so they master micro-habits that compound into real money. High earners? They often let lifestyle inflation eat their edge.

Let’s break down the 9 unbelievable ways this plays out, and how you can copy it starting today.

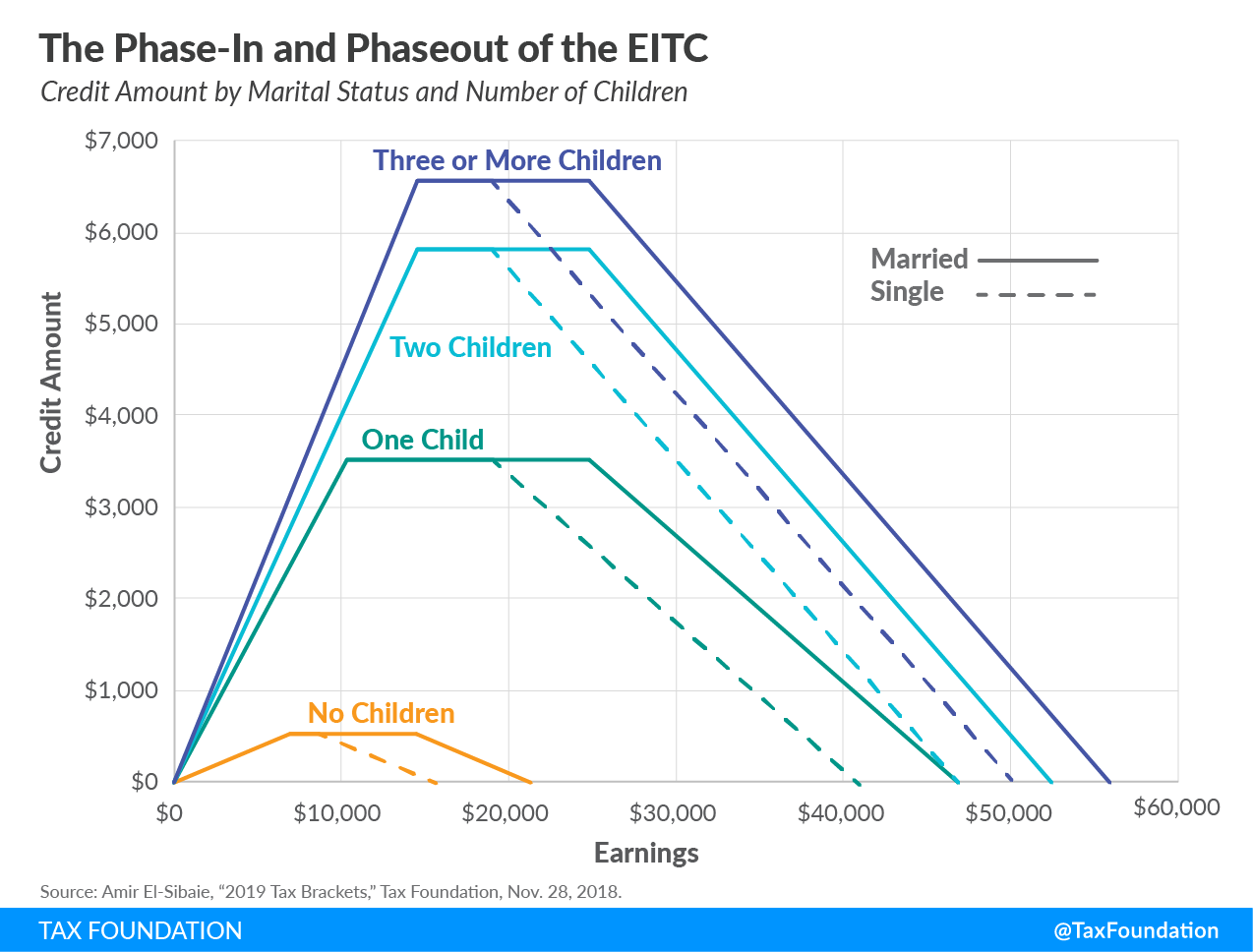

1. They Maximize Refundable Credits Like the EITC Without Even Trying

Low earners don’t chase obscure deductions, they qualify for powerhouse refundable credits that put cash directly in their pockets.

The EITC, for instance, can deliver up to $8,046 for families with three or more kids in 2025 returns filed this April. That’s money you get even if you owe zero taxes.

High earners? Their incomes push them past phase-out limits, so they miss out entirely.

One recent analysis notes how these credits turn tax filing into a savings windfall for modest households. No wonder April feels like bonus day for them.

2. Over-Withholding Becomes Their Accidental Savings Plan

Many tiny-salary workers have just enough withheld from modest paychecks to cover taxes—with a nice cushion left over.

When new tax breaks (like expanded child credits or tip/overtime deductions under recent laws) kick in but withholding tables lag, that extra withheld money comes roaring back as a refund.

High earners often adjust W-4s to minimize refunds, preferring steady paychecks. But that means no big April surprise deposit.

The hidden rule here: Treating over-withholding like a forced savings account works wonders when discipline is your daily reality.

3. Frugal Habits Turn Every Penny Into a Savings Superpower

People on tight budgets already know the drill, no impulse buys, meal prepping, and hunting deals become second nature.

In April, that discipline pays off big when refunds hit. They don’t blow it; they stash it or pay down debt that was quietly draining them.

High earners? Lifestyle creep sneaks in, bigger house, fancier car, daily lattes. Studies on spending behavior show low savers (often higher earners in disguise) spend 2-3% more of their salary on housing, transport, and food.

The result? Tiny-salary folks end up with higher effective savings rates relative to their means.

4. They Use the “Pay Yourself First” Rule Relentlessly

Even on a small salary, many low earners automate tiny transfers to savings the day payday hits.

It’s the hidden rule high earners ignore because “I’ll save later” feels safe when cash flow is strong.

But April tax refunds supercharge this: Low earners treat the lump sum as found money and funnel it straight into emergency funds or high-yield accounts.

Behavioral finance research backs it, optimism about the future boosts saving most among lower-income groups.

5. Tax Season Forces a Budget Reset They Actually Stick To

Filing taxes in April creates a natural money audit for everyone, but tiny-salary households treat it like a yearly reset button.

They track every expense because they have to. High earners often skip detailed reviews until something hurts.

This annual habit means they spot leaks faster and redirect refunds into real savings instead of lifestyle upgrades.

6. Community and Shared Resources Stretch Their Dollars Further

Low-income families often tap mutual aid networks, tool libraries, or family hand-me-downs, free ways to cut costs that wealthier people overlook.

In April, that mindset carries over: Refunds go further because baseline expenses stay low.

One expert roundup of frugal hacks highlights how under-$50 upgrades (like reusable items) save exponentially more for those already living lean.

High earners pay for convenience and miss the compounding effect.

7. They Avoid the “Keeping Up With the Joneses” Trap Entirely

No pressure to match neighbors’ vacations or cars when your circle lives similarly.

This frees up mental space, and actual cash, for saving.

High earners face social and professional expectations that quietly erode savings. The wealth paradox hits hard: More income, but net worth lags because spending scales up faster.

Tiny-salary savers dodge this entirely, making April refunds feel like pure profit.

8. High-Yield Savings and Simple Automation Work Wonders on Small Balances

Even $50 a month compounds when parked in a high-yield account earning 4-5% instead of 0.33% at traditional banks.

Low earners who discover this (often during tax season) turn refunds into starter nests that grow quietly.

High earners assume big balances make rate shopping unnecessary, until inflation eats the difference.

The hidden rule? Small, consistent actions beat sporadic big swings.

9. Mindset Shifts Turn Scarcity Into a Savings Advantage

Living with less forces creativity: Side hustles, bartering, and future-focused thinking become habits.

Research shows subjective financial perception often matters as much as actual income for building savings.

In April, that positive money mindset means refunds get deployed strategically, not spent on fleeting highs.

High earners sometimes feel “rich enough” and delay saving, only to watch opportunities slip away.

Quick Comparison: Tiny Salaries vs. High Earners in April

Here’s a simple table showing how the hidden rule plays out in real numbers (based on IRS trends and behavioral studies):

| Aspect | Tiny-Salary Savers | High Earners | April Edge Winner |

|---|---|---|---|

| Refund Size (Avg.) | Often $3K+ boosted by EITC | Lower due to phase-outs | Tiny salaries |

| Savings Habit | Forced discipline + automation | Lifestyle creep common | Tiny salaries |

| Tax Credit Leverage | Max EITC & refundables | Mostly non-refundable deductions | Tiny salaries |

| Spending Behavior | Every dollar tracked | Convenience & social spending | Tiny salaries |

| Refund Deployment | Straight to savings/debt | Often lifestyle or “catch-up” | Tiny salaries |

| Effective Savings Rate | Higher relative to income | Lower % despite bigger dollars | Tiny salaries |

These patterns hold across recent filing seasons, proving the hidden rule isn’t myth; it’s mechanics plus mindset.

The Bottom Line: Steal This Hidden Rule Before April 15

People with tiny salaries aren’t magic, they simply live the hidden rule every day: Discipline, incentives, and simplicity create outsized wins.

You don’t need a pay cut to copy them. Start by checking your EITC eligibility, automating a small savings transfer, reviewing withholding, and treating this April refund (or any extra cash) as your new savings launchpad.

The clock’s ticking, file early, claim every credit, and turn tax season into your wealth-building season.

Share Now if this surprised you, and comment below: What’s one tiny change you’re making this April?

Your future self (and your wallet) will thank you. Let’s make this the year you save more, starting now.