INTRODUCTION:

30-Year Mortgage at 6.45% Sounds Cheap, But This Hidden Trap Could Destroy First-Time Buyers in 2026 (What Banks Won’t Tell You)

Imagine signing on the dotted line for your first home with a shiny new 30-year mortgage at 6.45%.

It feels like victory after watching rates spike above 7% just a couple years ago.

But here’s what the banks won’t tell you: that “affordable” rate is hiding a trap that could quietly wreck your finances by late 2026.

First-time buyers are walking straight into it right now.

Why the 30-Year Mortgage at 6.45% Feels Like a Deal, Until You Dig Deeper

Rates have eased from their 2023 peaks, and Freddie Mac’s latest data shows the 30-year fixed hovering right around 6.46% as of early April 2026.

To many first-time buyers, anything under 7% feels like a win, especially compared to the brutal 7.8% highs of recent memory.

Yet zoom out to the full picture from 2000 to 2025, and the story changes. Rates averaged 8% at the start of the millennium, dipped to historic lows near 3% in 2021, then climbed again.

Today’s 6.45% 30-year mortgage sits in a middle ground that masks the real pain: home prices have skyrocketed since those ultra-low-rate days.

A modest rate on a much bigger loan often means monthly payments that rival or exceed what buyers faced years ago.

:max_bytes(150000):strip_icc()/5-16-032160ac25f043c690b2038729d4eaab.png)

The hidden trap isn’t the rate itself. It’s everything the lender glosses over to get you to close, temporary incentives, upfront fees, and long-term costs that turn your “dream” payment into a budget nightmare.

Here are the seven sneaky ways this trap could destroy first-time buyers in 2026.

1. The Discount Points Trap That Inflates Your Upfront Costs

Banks love advertising that eye-catching 6.45% 30-year mortgage rate.

What they don’t shout from the rooftops? You often have to pay discount points, prepaid interest, to actually get it.

One point typically costs 1% of your loan amount and lowers your rate by about 0.25%.

On a $320,000 loan (after 20% down on a $400,000 home), that’s $3,200 per point, cash you might not have sitting around.

Many first-time buyers skip this detail during the excitement of pre-approval, only to discover at closing that the “great rate” requires thousands extra upfront.

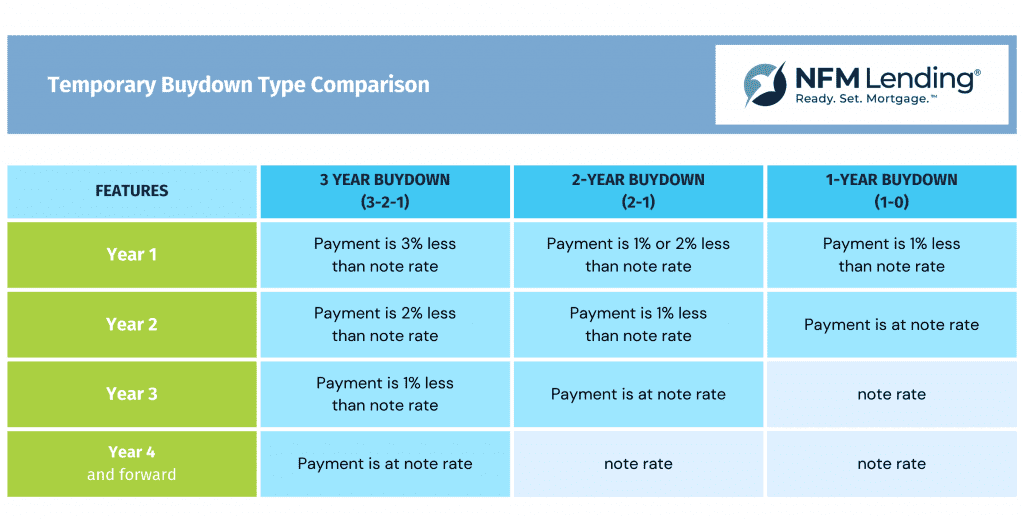

2. Temporary Buydowns That Set Up Payment Shock in 2026–2027

This is perhaps the sneakiest part of the 30-year mortgage at 6.45% trap right now.

Builders and sellers are aggressively offering 2-1 or 3-2-1 temporary buydowns to make your early payments look tiny.

Your rate might start 2–3% lower for the first year or two, dropping that monthly bill dramatically, then snap back to the full 6.45% (or higher) once the subsidy ends.

A buyer closing in spring 2026 could face a sudden $300–$500 jump in their payment by 2027 or 2028.

Lenders and builders push these hard because they help you qualify today, but the reset can destroy budgets that were already stretched thin.

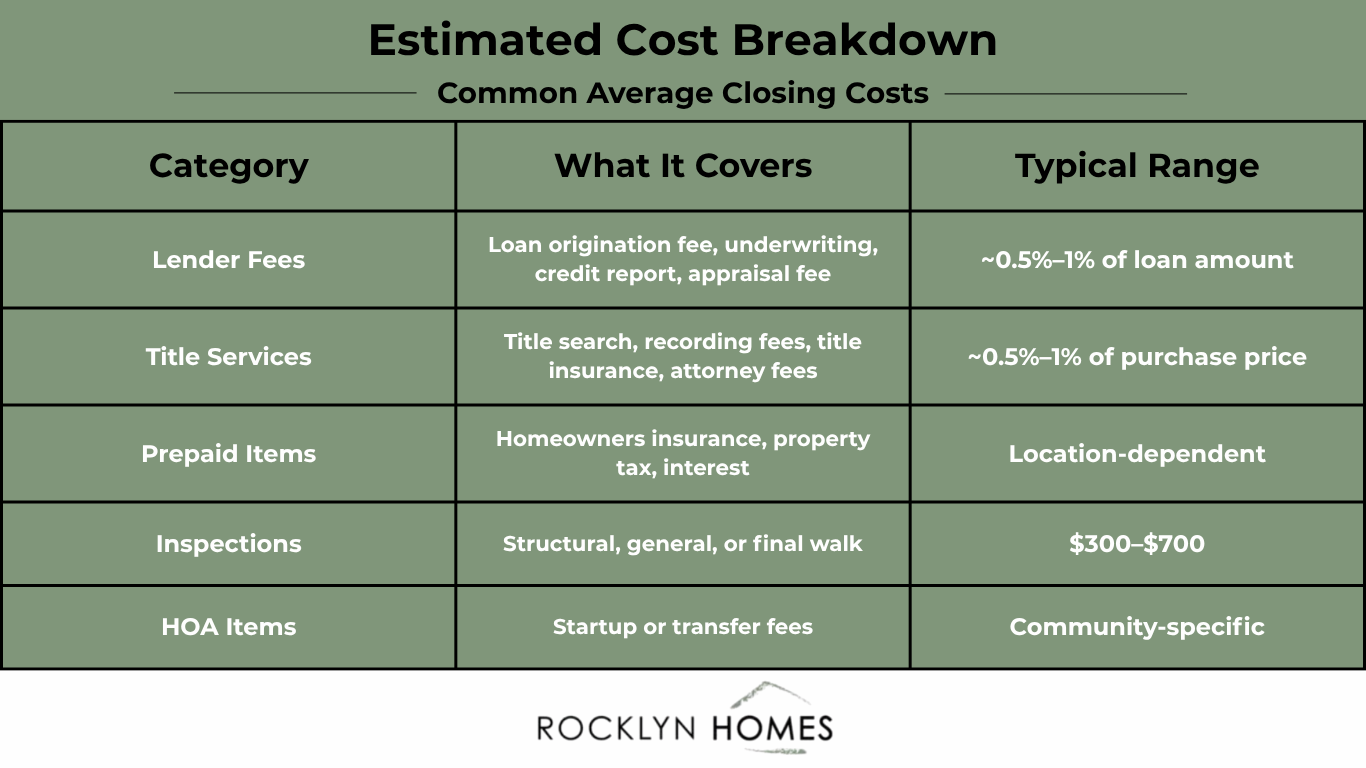

3. The No-Closing-Costs Illusion That Actually Costs You More

“No closing costs!” sounds amazing for cash-strapped first-time buyers.

In reality, the lender simply rolls those fees into your loan or charges a slightly higher rate.

Over the life of your 30-year mortgage at 6.45%, that “free” perk can add tens of thousands in extra interest.

It’s a classic trap that makes the deal feel easier upfront while quietly draining your wealth long-term.

4. Hidden Ongoing Costs That Turn Your Payment Into a Budget Black Hole

Your mortgage payment is only the beginning.

First-time buyers routinely underestimate the full cost of ownership.

Property taxes, homeowners insurance, and utilities can easily add $800–$1,500 monthly depending on location.

Then there’s maintenance, experts recommend budgeting 1–4% of your home’s value each year for repairs and upkeep.

On a $400,000 house, that’s another $4,000–$16,000 annually.

One broken HVAC system or roof leak can wipe out your emergency fund and force you to choose between fixing the house or making the mortgage payment.

5. Private Mortgage Insurance (PMI) That Lingers Longer Than Expected

If you put down less than 20%, PMI is required until you reach 20% equity.

At today’s higher home prices, building that equity takes longer than it did during the low-rate, low-price era.

You could pay hundreds extra each month for years on your 30-year mortgage at 6.45%, money that does nothing to build your wealth.

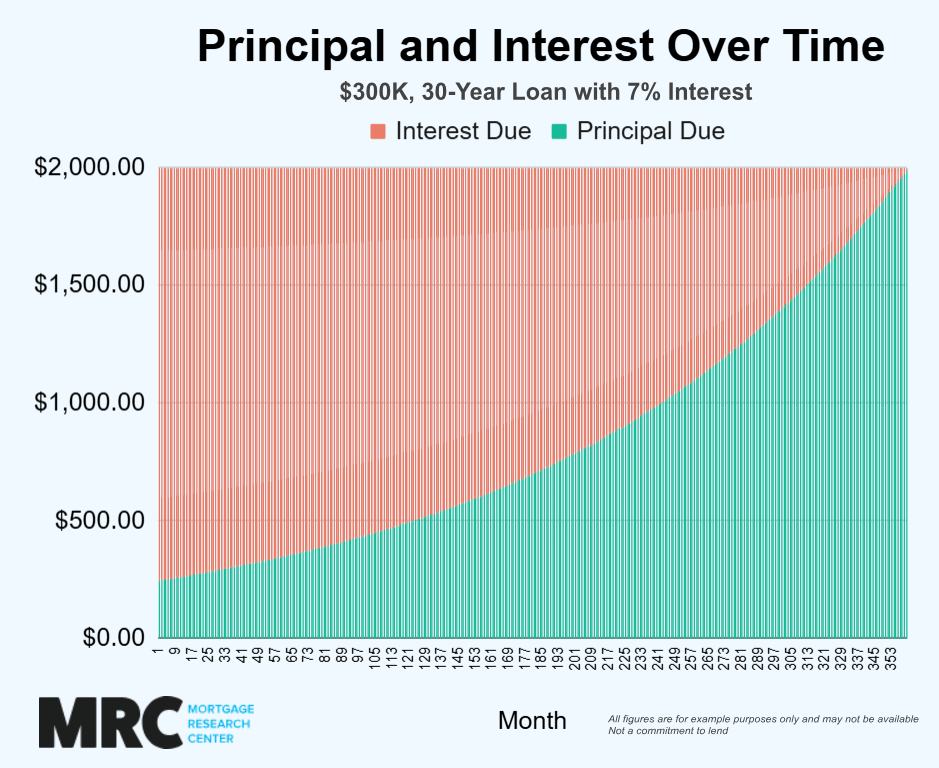

6. The Massive Lifetime Interest Drain Most Buyers Never Calculate

Here’s a gut-check most first-time buyers skip: on a $320,000 loan at 6.45%, you’ll pay nearly as much in interest as the original principal over 30 years—often $250,000–$300,000 or more.

That’s money you’ll never see again.

Banks won’t highlight the total cost because it makes the monthly number look far less appealing.

7. The Affordability Illusion That Leaves No Room for Life’s Curveballs

The 30-year mortgage at 6.45% qualifies you on paper, but stretch your debt-to-income ratio to the max and one job hiccup, medical bill, or car repair can push you toward foreclosure or forced sale.

First-time buyers often enter with zero cushion, assuming the “cheap” rate protects them.

It doesn’t.

Quick Comparison: How the Hidden Trap Plays Out in Real Numbers

To see the trap in black and white, here’s how different scenarios stack up for a typical first-time buyer (assuming a $400,000 home, 20% down, and average taxes/insurance):

| Scenario | Monthly P&I Only | Total Monthly (w/ Taxes, Insurance, PMI) | Upfront Extra Costs | 5-Year Payment Shock Risk | Lifetime Interest Paid |

|---|---|---|---|---|---|

| 30-Year Mortgage at 6.45% (No Buydown) | ~$2,010 | ~$2,900–$3,300 | $0–$6,400 (points) | Low | ~$280,000 |

| 2-1 Buydown (Temporary) | ~$1,650 (Yr 1) | ~$2,500–$2,900 (Yr 1) | $0 (seller pays) | High (jump in Yr 3) | ~$290,000+ |

| 2021 Low-Rate Era (3%, $300k home) | ~$1,265 | ~$1,900–$2,200 | Minimal | None | ~$155,000 |

| No-Closing-Costs Option | ~$2,050 | ~$2,950–$3,350 | Rolled into loan | Medium | ~$295,000 |

*Numbers are approximate based on current averages from Freddie Mac and Bankrate data. Actuals vary by credit, location, and lender.

These figures show why the 30-year mortgage at 6.45% can feel manageable at signing but turns destructive fast.

The Bottom Line: Don’t Let the Hidden Trap Destroy Your First Home

The 30-year mortgage at 6.45% isn’t inherently bad, but the way it’s packaged today creates a perfect storm for first-time buyers.

Temporary buydowns, hidden fees, and overlooked ongoing costs can turn excitement into regret within months.

Do your homework. Run the full numbers, including maintenance and taxes, before you fall in love with a payment that only looks affordable on paper.

Shop multiple lenders, ask pointed questions about buydowns and points, and build a healthy emergency fund before closing.

Your future self will thank you.

Share Now if you’re a first-time buyer eyeing the market in 2026, and drop a comment below: Which part of this hidden trap worries you most?

Knowledge is the only real protection against what banks won’t tell you.