$111,252 Income Shock: Why 73% of Americans Are Secretly Locked Out of Homeownership in 2026 (And No One Is Talking About This Hidden Trap)

Picture opening your paycheck and realizing the average home now demands $111,252 in annual income just to qualify.

That’s the $111,252 Income Shock staring down millions of families right now in 2026.

And the worst part? Nearly 73% of American households can’t clear that bar, according to the latest data.

No one is shouting about this hidden trap from the rooftops, but it’s reshaping the American Dream in real time.

The $111,252 Income Shock Explained: How We Got Here

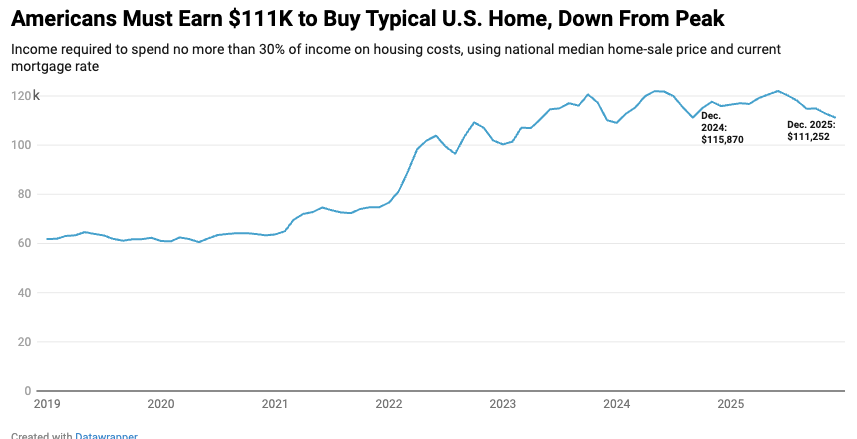

The numbers come straight from Redfin’s latest housing affordability analysis.

To afford the typical U.S. home for sale, median price around $426,747, you need to earn $111,252 a year while keeping housing costs under 30% of your income.

That covers mortgage, taxes, and insurance at today’s rates near 6.1%.

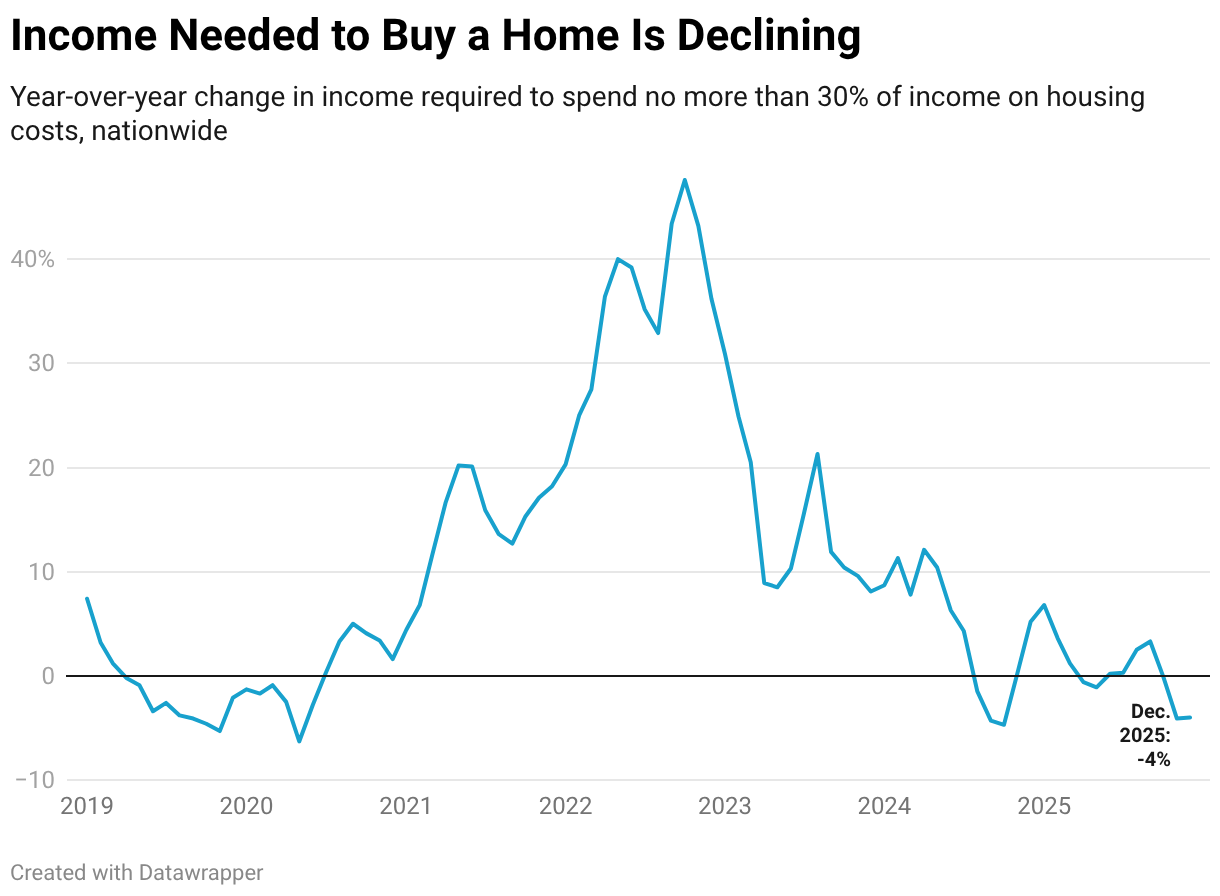

It’s down 4% from last year, which sounds like progress.

Yet the typical household earns just $86,000–$87,000.

That $25,000 gap is the $111,252 Income Shock in action.

And it’s not just theory.

Redfin notes the figure peaked above $122,000 mid-2025 before rates eased slightly.

Still, for most families, the math simply doesn’t work.

Why the $111,252 Income Shock Leaves 73% of Americans Locked Out

The National Association of Home Builders (NAHB) puts it even more starkly.

Their 2026 priced-out analysis shows roughly 65%–75% of U.S. households (depending on new vs. existing homes) simply can’t qualify for the median property.

Earlier data pegged it at 74.9% for new homes at higher rates, close enough to the 73% figure echoing across reports.

That means over 100 million households are mathematically sidelined.

Only 12 out of 50 major metro areas have median homes affordable at the national median income.

The rest? Off-limits.

This isn’t a temporary blip.

It’s a structural trap built on high prices, stubborn rates, and wages that haven’t kept pace.

The Hidden Traps Behind the $111,252 Income Shock No One Discusses

Most headlines talk about “high rates” or “prices.”

But the $111,252 Income Shock hides deeper mechanisms quietly draining opportunity.

Here are the seven real traps pushing 73% of Americans to the sidelines.

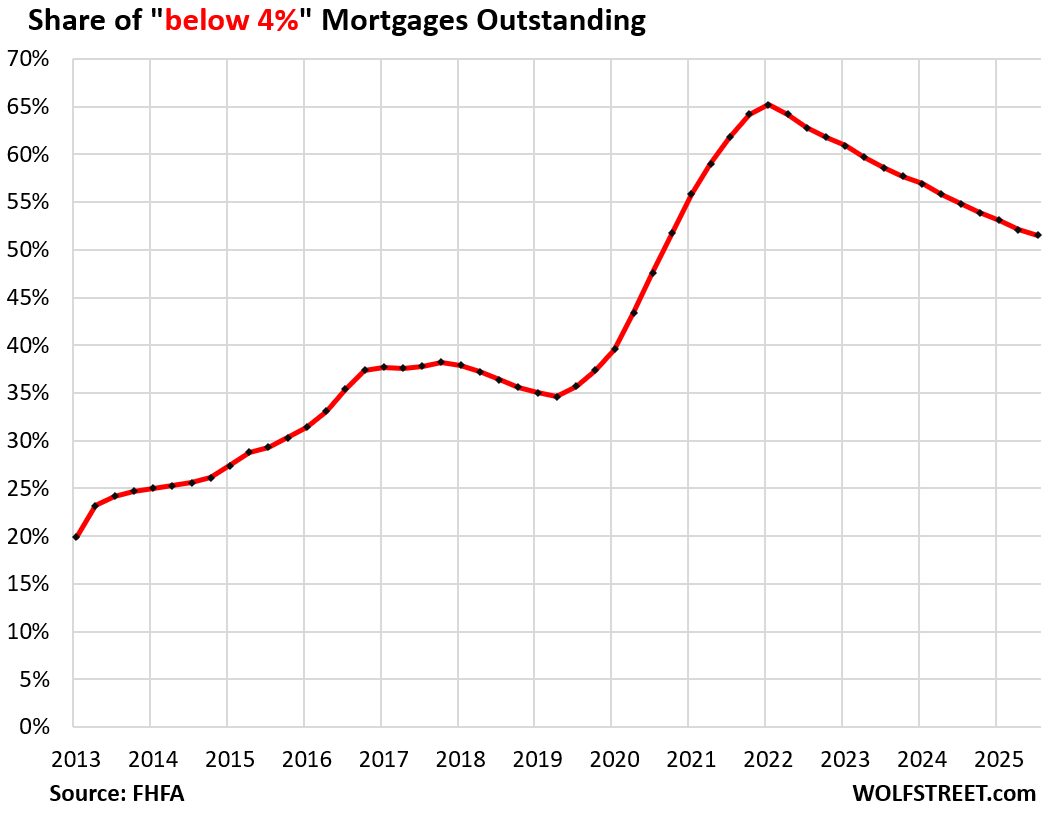

1. Mortgage Lock-In Freezing Inventory and Driving Prices Higher

Existing homeowners with sub-4% rates refuse to sell.

Storable’s 2026 Moving Forecast reveals 73% would only move if they could transfer their rate.

That locks up supply.

Fewer homes on the market means bidding wars and inflated prices, even as new construction lags.

Your dream starter home stays out of reach because sellers won’t budge.

2. The Down-Payment Wall Most Families Can’t Climb

Even if you hit the $111,252 Income Shock threshold on paper, 20% down on a $427,000 home is $85,000 cash.

Add closing costs and you’re looking at six figures upfront.

For the 73% below that income line, saving that much feels impossible while rents consume 30–50% of paychecks.

The trap? Lenders approve the loan but you never reach the closing table.

3. Debt Load That Quietly Lowers Your Qualifying Power

Student loans, car payments, credit cards, they all count against your debt-to-income ratio.

Many millennials and Gen Z carry $30,000+ in student debt alone.

That slices thousands off what you can borrow, pushing the effective income needed even higher than $111,252.

The $111,252 Income Shock doesn’t account for your existing bills, but banks sure do.

4. Wage Stagnation vs. Exploding Housing Costs

Median wages rose modestly, but home prices surged 150% since 2005 while incomes grew just 28%.

The gap compounds yearly.

Even with slight 2026 relief, the $111,252 Income Shock remains 30% above what most households bring home.

No one talks about how inflation in groceries and health care steals the extra dollars you’d save for a house.

5. Investor Competition Snapping Up Starter Homes

Corporations and cash buyers scoop up entry-level properties, converting them to rentals.

This reduces supply for first-time buyers and keeps prices elevated.

The result? The $111,252 Income Shock feels even heavier because the homes you can afford on paper simply aren’t available to regular families.

6. Regional Disparities That Trap You in High-Cost Areas

In San Jose you need nearly $460,000 income.

In Pittsburgh? Just $64,000.

Yet jobs cluster in expensive metros.

Moving for affordability means leaving career growth behind.

The $111,252 Income Shock hits hardest where opportunity lives.

7. Psychological and Timing Traps Delaying the Dream Indefinitely

Fear of layoffs, economic uncertainty, and “waiting for rates to drop more” keep people renting longer.

Redfin’s economist Chen Zhao notes nerves about job security are a major obstacle even as numbers improve slightly.

The longer you wait, the higher prices climb, and the $111,252 Income Shock compounds with lost equity.

Quick Comparison: The $111,252 Income Shock Across America

To make the trap crystal clear, here’s how the numbers stack up:

| Metro Area | Income Needed for Median Home | % of Local Households Priced Out | Key Trap Highlight |

|---|---|---|---|

| National Average | $111,252 | ~73% | Wage gap + low inventory |

| San Jose, CA | $458,504 | 86%+ | Extreme regional disparity |

| New York City | $200,280 | 78% | Debt + high living costs |

| Pittsburgh, PA | $64,106 | Under 40% | Rare bright spot for affordability |

| Seattle, WA | ~$180,000 | 72% | Investor competition heavy |

(Data synthesized from Redfin 2026 and NAHB 2026 analyses; only 12 metros fall within national median income reach.)

These figures show why the $111,252 Income Shock isn’t uniform, it’s a nationwide crisis with local landmines.

What This Means for Your Future, and the American Dream

The $111,252 Income Shock isn’t just a statistic.

It’s delaying marriages, postponing kids, and forcing multi-generational living for millions.

First-time buyer share has dropped roughly 50% since 2007.

Homebuyer median age now hovers near 59.

Yet the door isn’t fully slammed shut.

Slight rate relief and more negotiating power in 2026 create a narrow window, if you act strategically.

Smart Moves to Beat the $111,252 Income Shock

• Boost income through side hustles or career jumps before rates shift again. • Attack debt aggressively to improve your DTI ratio. • Target affordable metros or emerging suburbs with strong job growth. • Explore first-time buyer programs, down-payment assistance, or FHA loans that lower the cash barrier. • Build a dedicated house fund even while renting—every dollar compounds. • Monitor local inventory weekly; the right home at the right moment can still beat the trap.

The $111,252 Income Shock rewards preparation, not patience.

The Bottom Line: Don’t Let the $111,252 Income Shock Steal Your Future

73% of Americans are quietly locked out today, but that doesn’t have to include you.

The hidden traps are real, yet awareness is the first step toward breaking free.

Model your numbers, talk to a lender this month, and start building equity however you can.

The American Dream of homeownership hasn’t vanished, it’s just evolved into a tougher challenge that rewards the informed.

Share Now if this $111,252 Income Shock opened your eyes.

Drop a comment: What’s your biggest hurdle right now, down payment, rates, or something else?

Your story might help someone else dodge the trap.

Read on for more housing insights, and let’s keep the conversation going before 2027 makes it even harder.